Daily Commentary (17-Feb): Mixed INDOGB, with Longer Tenors Up; 2021 Current Account Balance Expects Surplus

admin | Posted on |

On Wednesday, INDOGB was mixed, while the JCI and rupiah against USD fell after two days of sharp increase. The JCI fell 0.2% to 6,835.1 (+3.1% MTD or +3.9% YTD), but foreign investors kept reporting net inflow, reaching Rp649.6bn (inflow of Rp12.3tn MTD or +Rp18.4tn YTD). Asian equity indices also closed mixed as investors continued to monitor geopolitical tensions between Russia and Ukraine. The Hang Seng index was up 0.3% to 24,792.8 (+6% YTD), while the Nikkei index fell 0.8% to 27,232.9 (-5.4% YTD). On the same day, the rupiah depreciated by 0.4% to Rp14,318/USD (still appreciated by 0.5% MTD or depreciated by 0.5% YTD).

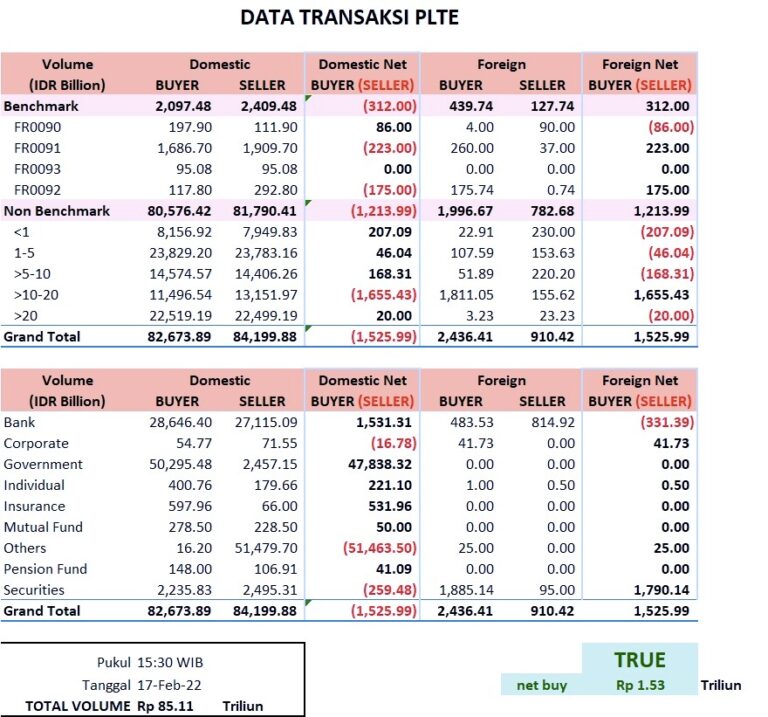

INDOGB was mixed, with the longest benchmark bond prices up, sending bond yield lower. Foreign investors still reported net buy, at Rp1.5tn, mostly from non-benchmark series (+Rp3.2tn), based on CTP PLTE data. This marks the eighth consecutive day of foreign inflows, totaling Rp10.5tn. According to Bloomberg, the 5-yr FR90 benchmark series traded at 99.17 (-0.03%) or yielded 5.31 (+0.6 bps)%, the 10-yr FR91 at 99.09 (+0.02%) or yielded 6.5% (-0.3 bps), the 15-yr FR93 at 99.98 (-0.04%) or yielded 6.48% (+0.5 bps), and the 20-yr FR92 at 102.47 (+0.15%) or yielded 6.9% (-1.4 bps). Meanwhile, regarding the 10-yr RoI USD global bond that will mature in Mar-2031, its price fell slightly to 92.15 (-0.07%), yielding 2.84 (+1 bps), and the 5-yr CDS went up slightly to 96.71 (+1.9 bps).

The latest DMO bond flow data was as of 16-Feb (reflecting trading on 14-Feb), wherein foreign ownership in government bonds went up to Rp894tn or 19% of the total outstanding (inflow of Rp6.72tn MTD or +Rp1tn YTD). YTD, the biggest net buyer of government bonds (incl. sukuk) is Bank Indonesia at Rp154.9tn (from SKB III burden-sharing at Rp157tn in Dec-2021, with settlement date on 3-Jan-2022), followed by insurance & pension fund at Rp37.8tn. Retail and other investors also reported net buys at Rp5.8tn and Rp13.3tn, respectively. With PBS002 maturing, onshore banks became a net seller at Rp18.8tn YTD.

Indonesia’s 4Q 2021 current account will be released on Friday. Bank Indonesia estimates there will be a current account surplus in 2021 of around 0.3% of GDP (vs. -2.7% of GDP in 2020). In 3Q2021, Indonesia’s current account surplus increased to USD 4.47bn or equivalent to 1.5% of GDP as the goods surplus widened sharply to USD 15.03bn from USD 9.79bn a year ago amid a further recovery in global demand and surging commodity prices, while the secondary income surplus inched up to USD 1.42bn from USD 1.37bn a year earlier. On the other hand, the primary income gap rose to USD 8.34bn from USD 7.40bn, while the services shortfall increased to USD 3.63bn from USD 2.76bn.

(Source: Mandiri Sekuritas)

Leave a Reply